interest rate hikes and the uncertainties around the US and UK credit crunch have taken their toll. Things are not likely to improve for some time. Most people expect prices to stagnate but the doom-mongers are out in force and many people are again talking of a house price crash.

interest rate hikes and the uncertainties around the US and UK credit crunch have taken their toll. Things are not likely to improve for some time. Most people expect prices to stagnate but the doom-mongers are out in force and many people are again talking of a house price crash.In the last few years, we have been advising investors to buy in London – prices have risen 25% in the last two years and ca. 50% in the West End. But we now do not see any significant growth in 2008. There are risks of a fall in prices - so for new investors, now is not the time to buy. For established investors with much equity and cash, bargains could be available in the next few months as the market cools further.

We do not expect a crash for the following reasons:

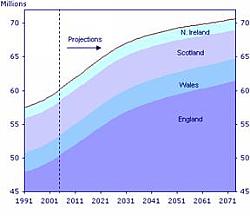

- Shortage of supply – this is an underlying trend and it's not likely to go away with an expanding population, smaller families, more singles and people's continued aspirations to live in a home, many on their own. We believe 300,000 new homes need to be built per year to keep up with demand, with the biggest demand being in London and southern England, but only 200,000 are being built, mostly in other parts of the UK.

- Employment – unemployment has remained stable a 5.4% - barring a recession, this should protect against too many distressed households.

- Interest rates – these are likely to begin dropping either early December or more likely in January 2008. A 0.25% drop is likely in the next three months, with another 0.25% drop in mid 2008. This should ease household finances – the Bank of England cannot afford to see a wholesale house price crash – so expect them to react to house prices like they have done when prices have been rising strongly.

- Inflation – despite record oil prices close to $100/bbl, inflation (measured in CPI) has remained remarkably low. This allows room to drop interest rates.

- GDP – this is expected to slow to 2% or slightly below in 2008 and will further encourage the Bank of England to drop rates, which should in turn help support house prices.

- Sterling – the pound is likely to drop as oil prices rise and interest rates come down slightly – this should increase manufacturing competitiveness boosting exports and manufacturing jobs, but the threat is increased inflation. As long as inflation remains in control and wage inflation subdued as it currently is, Sterling will probably correct against the Euro and possibly against the Dollar though this should not unduly affect property prices.

- Immigration – record levels of inward migration is boosting the UK's population and keeping wage inflation lower than it normally would be – both these boost property prices and should help prevent a fully fledged crash.

- Tax – the flat capital gains tax change to 22% should positively impact the market and increase returns for investors.

|  |

We expect the GDP in northern parts of the UK and the Midlands to drop to 1% whilst London will continue to motor along at about 2.5%. The lack of new public sector jobs and pressure on manufacturing will suppress property prices in these northern areas. The population is growing at a slower pace, less services jobs are available and it's easier to build new homes – so the north should feel the effects of the interest rates more than the south. This is why we were not surprised to see the recent Rightmove.co.uk report which showed London prices rising 2.3% in a month whilst all other areas saw falls of up to 2%.

The wild card continues to be the oil prices – and as we have so often predicted, we believe it will end 2008 at $125/bbl. The big unknown is whether this will affect inflation – it seems rising from $20/bbl to $95/bbl has had no appreciable affect on longer term inflation, so we are now thinking that a rise to $125/bbl may not be a tipping point. If you are concerned about oil prices, you'd better read all our special reports on the subject.

The wild card continues to be the oil prices – and as we have so often predicted, we believe it will end 2008 at $125/bbl. The big unknown is whether this will affect inflation – it seems rising from $20/bbl to $95/bbl has had no appreciable affect on longer term inflation, so we are now thinking that a rise to $125/bbl may not be a tipping point. If you are concerned about oil prices, you'd better read all our special reports on the subject.

As a reminder, we enclose our ranked list of the best towns and cities to invest in – the top two are both exposed positively to higher oil prices:

Highest growth

- London

- Aberdeen (oil town)

- Cambridge

- Reading

- Bristol

- Brighton

- Plymouth

- Portsmouth

- Southampton

- Manchester

- Leeds

- Bradford

- Chester

- Glasgow

- Oxford

- Edinburgh

- Leicester

- Liverpool

- Derby

- Birmingham

- Middlesboro

- Hull

- Nottingham

- Newcastle

Lowest Growth

So all investors – be careful – make sure you have enough cash to weather some rough times and be on the lookout for bargains from distressed sellers. Some people simply have to move to a new location of work or move because of divorce or other problems, so do not underestimate how much reduction you could get if you are able to move quickly and have proper financing in place. For the less wealthy investors – it's probably best to hold fire for now and monitor the market. For the first time buyer – best not enter the market just at this time for fear of immediately running into negative equity.

But remember, if we'd all listened to those Chicken Little's who predicted a house price crash back in 2001, we'd have missed out on a doubling and in some casing trebling of house prices. Confidence has been shaken and prices can go in both directions, so it's up to you to judge whether you want to enter this market and seek out bargain, or sell your portfolio because you are so spooked. But the wealthiest investors normally buy on a low and hold – Warren Buffet being the classic example – of a disciplined value investor. We can try and follow his tenants. But don't expect to make serious money unless you risk at least some of your hard-earnt cash.

|  |

Oil Prices Continue to Skyrocket

On 14 th August when oil prices were at $70 / bbl – we predicted oil prices would rise to $125 / bbl by end 2008. They almost touched $100/bbl end November before easing back to $90/bbl. We have written ten special reports on this topic – we suggest all serious property investors should read these report that have taken years of analysis and insights to prepare:

- 169: Oil supply crunch begins… protect yourself

- 168: Alarm bells ringing – oil price shock now on the horizon

- 163: Making Serious Money as asset prices plateau – resources and property

- 161: Resources winners and losers - ranked list for property investors

- 160: Find out the winners and losers in the biggest oil boom in history - about to happen...

- 159: Massive oil boom - the winners and losers - be prepared

- 158: Supply and demand scenarios - oil boom and the property investors insights

- 157: Impact of "Peak Oil" for Property Investment

- 151: Oil price $125 / bbl and rising…how to take advantage in property

- 150: Peak Oil shortly due to be reach – unique insights for a property investor

- 148: Take advantage of the oil/gas/coal boom – key insights

In these reports, you'll find, for free, all you need to know about how to make serious money from the predicted boom in oil prices. The analysis of all producing oil nations has taken years to prepare and we finally think we've cracked it. The results shows that we are now on a rolling plateau production rate, meanwhile demand is increasing by 1.3 million barrels a year. We spotted this abnormality on 7th June 2007 and we now think prices will skyrocket. The opening gaps between oil supply and oil demand is a dangerous situation. OPEC meet early December and may very well communicate they will increase supply by 0.5 million bbls oil per day. But it's too little too late. Any increase in oil supply will likely be lower value high sulphur heavy crude. When the markets finds out that the global oil producers cannot increase production any further, there will be a mother of all oil price hikes. So be prepared. And don't say we didn't warn you!

|  |

This analysis is underpinned by our unique oil production mathematical model which forecasts every country's production up until 2015 and it does not make very pleasant reading. As already described – production is on a plateau and has been on plateau since October 2005. This is why prices are rising. But many in the market mistakenly believe there is more oil out there that can be switched on – it's not going to happen. The plateau could be long and undulating, but we believe everyone is more or less pumping at their maximum. So for the property investor:

- do not purchase property in far off places which take a tank full of gas to reach – this includes suburban homes with a very long daily commute to work centres

- be careful about purchasing holiday homes in places that need a 10 hour flight to reach (stay within 2-3 hour flight radius from major population centres)

- be careful not to purchase huge fuel inefficient homes in cold climates requiring much heating oil, gas or electric

- the lowest risk options are city central quality apartments close to services jobs

- consider purchasing property:

- in oil, coal, gas and mining boom towns (refer to the above special reports)

- close to oil company and oil services company offices

- in areas positively affected by renewable energy developments – solar, wind, hydro-electric, low energy conservation centres.

For US investors the best places to invest in the USA to take advantage of the oil boom are:

- Wyoming – Green River area for the coal boom

- Western Colorado – oil shale potential future boom area

- Texas – Houston, and Dallas-Irving-Fort Worth – oil/gas HQs and technical services centres

- New York City – oil/gas/energy trading

- Oklahoma – ethanol from corn and some old oil/gas wells

The USA has more coal than any other country in the world. So it seems clean coal technology with electricity to automobiles (electric cars) will be a key future response to dwindling oil (and gas) supplies.

As we predicted, Houston has done well in the last few years to weather any downturn in the real estate market and we expect this to continue. But be very careful not to purchase property more than a 30 minute auto commute to a city centre – when oil prices skyrocket, people will want to move into the cities to reduce their fuel bills. Outlying suburban areas will suffer. An extreme example is – don't buy a large detached suburban house 80 minutes commute to downtown Detroit. The gasoline guzzling car plants will close. No-one will be able to afford to commute or heat a huge house in the cooler north. You would be better off buying a downtown apartment in the oil capital of the USA – Houston, which will benefit from the high oil prices that in turn will destroy the gas guzzling autos.

|  |

US Market Update

The US real estate market continues to be in a distressed and depressed position in most states. However, the market varies – the US is such a huge market – some areas are still rising but overall the situation looks fairly bleak. We believe the extent of the unraveling of the sub-prime woes is about 45% complete. In Spring 2008 we will be past the peak of the rates resetting and by September 2008 most of the resetting will have unraveled. Until then, expect a bumpy ride with continuous negative headlines and some banks getting into trouble and writing down bad debt. The problem emerged in the open in July – it's now December so quite some time has now passed.

![[Reset]](http://www.propertyinvesting.net/images/newsletter/Nov07-image021-200.gif) US homes prices have been most negatively affected in areas away from cities where prices shot up the most. Examples are holiday areas in California and Florida. But closer scrutiny of the numbers identified that cities like Miami and Detroit actually saw prices rise slightly in the last quarter. Prices in large cities like New York and Los Angeles are fairly stable. Prices in Texas have been robust and in most areas rising. Prices in remoter areas with less service industries and more manufacturing and agriculture have generally dropped back. It's difficult to generalize but it does not look like a full scale meltdown. Although

US homes prices have been most negatively affected in areas away from cities where prices shot up the most. Examples are holiday areas in California and Florida. But closer scrutiny of the numbers identified that cities like Miami and Detroit actually saw prices rise slightly in the last quarter. Prices in large cities like New York and Los Angeles are fairly stable. Prices in Texas have been robust and in most areas rising. Prices in remoter areas with less service industries and more manufacturing and agriculture have generally dropped back. It's difficult to generalize but it does not look like a full scale meltdown. Although  everyone talks about the US housing bubble and it's bursting, prices rose by a relatively modest (in global terms) 50% in five years up until early 2007. It's difficult to see how prices could crash and burn when home prices came from a low base.

everyone talks about the US housing bubble and it's bursting, prices rose by a relatively modest (in global terms) 50% in five years up until early 2007. It's difficult to see how prices could crash and burn when home prices came from a low base.

The US population has risen from 150 million in 1950 to 300 million today. The population  is projected to rise to 450 million by 2050. This implies 75 million new homes will be required. The fastest growing areas are Nevada, Arizona, Texas, California and Florida – see our special reports for more details. So in these areas where land shortages occur, it is likely prices will recover and move far higher in years to come. One can expect a period of stagnation for a few years then prices in these areas will again rise. California should also follow suit as the population in this state is also increasing and it's difficult to see where all the new homes will be build with increasing environmental restrictions coming into force. Ditto Florida. And remember the wave of aging babyboomer that will start retiring this year, peaking in 2016.

is projected to rise to 450 million by 2050. This implies 75 million new homes will be required. The fastest growing areas are Nevada, Arizona, Texas, California and Florida – see our special reports for more details. So in these areas where land shortages occur, it is likely prices will recover and move far higher in years to come. One can expect a period of stagnation for a few years then prices in these areas will again rise. California should also follow suit as the population in this state is also increasing and it's difficult to see where all the new homes will be build with increasing environmental restrictions coming into force. Ditto Florida. And remember the wave of aging babyboomer that will start retiring this year, peaking in 2016.  These people will want to move to the sand, sea, surf and cultural centres. This is why we have a long term view that coastal Florida, California and culturally interesting places like Austin in Texas and Sante Fe in Utah will continue to see prices rising after a few years.

These people will want to move to the sand, sea, surf and cultural centres. This is why we have a long term view that coastal Florida, California and culturally interesting places like Austin in Texas and Sante Fe in Utah will continue to see prices rising after a few years.

But be careful investing in oil intensive areas like Detroit and Cleveland. These cities are far too reliant on the auto-industry and the increase in oil prices will hit them hard. But Houston will prosper along with the new energy corridor of western Colorado, Wyoming and NE Utah – areas expose to coal, oil shale and coal-bed methane and closer to the Oil Sands projects of Alberta in Canada.

Property prices have risen dramatically in the last seven years as interest rates have remained low and inflationary pressures subdued. The GDP of Europe has averaged around 2% for the last few years. But Euro area asset prices are likely to come under pressure as evidenced by price drops in Ireland this year. It's late in the party and we would steer clear of faltering economic area exposed to high oil prices such as Italy, Portugal and Greece. Southern Spain and southern France will likely see prices continue to increase led by wealthy people migrating to these area and setting up businesses – populations in areas like Perpignan, Toulouse, Sete and Montpellier in France and Marbella, Malaga and Valencia in Spain are increasing - investment levels remain robust. Wealthy retiring northern European baby-boomers will also support this market.

Germany is an interesting market but it's difficult to judge whether it's best to invest in previously depressed cities like Berlin and eastern Germany where asset prices are very low priced, or areas like Munich in the wealthy south which have very high property prices. Our gut tells us, that Munich and the south is the better place because of the booming services business, pleasant climate, local wealth, central position and booming banking and high-tech businesses. But it's not an obviously a high return area and Germany has suffered in the last 15 years compared with countries like UK and Ireland because of the excessive regulation and high cost of labour. Undoubtedly a pleasant place to live, but it is difficult to see high investment returns. Yes, yields for rental property are high in northern and eastern Germany, but asset prices are unlikely to boom.

|  |

The new European Union entrants Romania and Bulgaria remain very interesting. We expect the markets to cool in the next year, but property prices in good locations in the capital cities of these two countries should continue to boom as long as their economies continue to be managed affectively. There has been a brain drain away from Romania and Bulgaria to places like the UK and Ireland in the last few years, but eventually these people will return flush with cash and want to purchase property in the capital cities Sophia and Bucharest, as well as nice farm houses in the best areas. So we expect prices to double or more in Romania in the next ten years. One just needs to be very careful with the legal, tax side and make sure one does not get ripped off!

Bratislava – the capital of Slovakia is another gem. It's only 60 km from Vienna and cross border trade is increasing rapidly. Austrian property prices have also risen by about 10% in the last year. We expect Bratislava prices to normalize towards Vienna prices in future years. It's very central and the flat tax regime plus car plants on Slovakia have helped the economy enormously – worth checking out for all those exploratory investors in Europe. Another interesting option is ski villas in the High Tratras mountain – a booming ski centre – though one needs to research the affects of global warming since the snow might become rare in future years. But still a beautiful scenic area for holidays years round.

|  |

Norway : If one uses these criteria for cities like Bergen in Norway it's difficult to see how prices would not continue rising. London is the same – it's also a global centre of oil and commodities financing and re-investment of proceeds from the extractive industries that are booming. Moscow is similar albeit more regional in its sphere of influence.

Norway : If one uses these criteria for cities like Bergen in Norway it's difficult to see how prices would not continue rising. London is the same – it's also a global centre of oil and commodities financing and re-investment of proceeds from the extractive industries that are booming. Moscow is similar albeit more regional in its sphere of influence.  South Africa : Localized gems occur such as Rustenburg to the west of Pretoria in South Africa. The population is booming as 25,000 new jobs are being created in the expanding platinum and chrome mines. Pretoria is also worth considering with its access to Johannesburg government employment – it is the regional centre of the Bushveld Complex of minerals and mines, with most mines within a 100 km radius of the city.

South Africa : Localized gems occur such as Rustenburg to the west of Pretoria in South Africa. The population is booming as 25,000 new jobs are being created in the expanding platinum and chrome mines. Pretoria is also worth considering with its access to Johannesburg government employment – it is the regional centre of the Bushveld Complex of minerals and mines, with most mines within a 100 km radius of the city.  Canada : Fort McMurray in NE Alberta, Canada is booming oil town. A huge wave of new jobs have been created in the oil sands business – accommodation is desperately short and rentals are in big demand. Many billions of dollars are being invested to grow oil sands production – in part because this makes the USA less reliant on overseas imports. This is something not likely to go away – hence Fort McMurray will likely see prices booming into the future. Calgary the centre and HQ of the Canadian oil & gas business is another booming town – and a pleasant place to live as well. The creation of new oil and gas jobs and wealthy retiring oil workers will likely support prices into the next decade.

Canada : Fort McMurray in NE Alberta, Canada is booming oil town. A huge wave of new jobs have been created in the oil sands business – accommodation is desperately short and rentals are in big demand. Many billions of dollars are being invested to grow oil sands production – in part because this makes the USA less reliant on overseas imports. This is something not likely to go away – hence Fort McMurray will likely see prices booming into the future. Calgary the centre and HQ of the Canadian oil & gas business is another booming town – and a pleasant place to live as well. The creation of new oil and gas jobs and wealthy retiring oil workers will likely support prices into the next decade. USA : The Green River area of Wyoming is another gem – who would believe that in 2007, a boom is taking place in a coal mining area in the USA? This part of the world has more barrels of oil equivalent of hydrocarbons (locked up in coal) than Saudi Arabia and Russia combined. The USA will never be short of fuel for electric power station because some of these coal seams are 50 metres thick and mines are open-cast and of the highest quality anthracite coal. Huge wealth is being created as production is increased and this is supporting rentals and property prices in this remote area of the USA.

USA : The Green River area of Wyoming is another gem – who would believe that in 2007, a boom is taking place in a coal mining area in the USA? This part of the world has more barrels of oil equivalent of hydrocarbons (locked up in coal) than Saudi Arabia and Russia combined. The USA will never be short of fuel for electric power station because some of these coal seams are 50 metres thick and mines are open-cast and of the highest quality anthracite coal. Huge wealth is being created as production is increased and this is supporting rentals and property prices in this remote area of the USA.  London and New York – examples: Ever wonder why property in central London and Manhattan are so expensive? Because of wealth and amenities. The wealth is from businesses, private investors, shareholders and corporate headquarters – financial, banking, services jobs. But the reason why so many people want to pay huge prices for such property is because of the local amenities. Shops, theatre, trains, planes, work-offices, tubes/metro, roads, restaurants. Proximity to high paid jobs, where profits are made and a nice residential environment are key. So in London when you think of Mayfair it ticks all the boxes. So does Covent Garden. So does Kensington. But can prices in such areas go any higher? This depends on how successful the businesses close by are doing. London has been gaining relative ground on New York as a premier global financial centre – in part because it is less regulated and in part because of the huge wave of Middle Eastern, Asian and Africa money that has found its way to London – a truly cosmopolitan global city. So if you think global finance stimulated by China India and the Middle East will prosper, buying property in Mayfair could still be good value for money.

London and New York – examples: Ever wonder why property in central London and Manhattan are so expensive? Because of wealth and amenities. The wealth is from businesses, private investors, shareholders and corporate headquarters – financial, banking, services jobs. But the reason why so many people want to pay huge prices for such property is because of the local amenities. Shops, theatre, trains, planes, work-offices, tubes/metro, roads, restaurants. Proximity to high paid jobs, where profits are made and a nice residential environment are key. So in London when you think of Mayfair it ticks all the boxes. So does Covent Garden. So does Kensington. But can prices in such areas go any higher? This depends on how successful the businesses close by are doing. London has been gaining relative ground on New York as a premier global financial centre – in part because it is less regulated and in part because of the huge wave of Middle Eastern, Asian and Africa money that has found its way to London – a truly cosmopolitan global city. So if you think global finance stimulated by China India and the Middle East will prosper, buying property in Mayfair could still be good value for money. location', as they say. Never forget this. If you find a location very close to excellent amenities that you believe will have increasing numbers of wealthy residents and is under-valued, go for it! Some examples in London are:

location', as they say. Never forget this. If you find a location very close to excellent amenities that you believe will have increasing numbers of wealthy residents and is under-valued, go for it! Some examples in London are: Luxemburg - another good example: And remember our analysis of Luxemburg? No other European city has such an exciting combination of land shortage, population growth, massive wealth and GDP growth – a lovely city to live in – some of the most wealthy Europeans will want to a place in this city tax haven and financial wealth centre.

Luxemburg - another good example: And remember our analysis of Luxemburg? No other European city has such an exciting combination of land shortage, population growth, massive wealth and GDP growth – a lovely city to live in – some of the most wealthy Europeans will want to a place in this city tax haven and financial wealth centre.  regularly – year-on-year. You won't find many advertising this fact though. Why should they? Most people don't like other people knowing how much money they have. The purpose of writing this closing contribution is to help you think about why you are investing in property. It's likely because you want to make serious money and it's probably because you enjoy it was well. So what an excellent combination. You like it and you make

regularly – year-on-year. You won't find many advertising this fact though. Why should they? Most people don't like other people knowing how much money they have. The purpose of writing this closing contribution is to help you think about why you are investing in property. It's likely because you want to make serious money and it's probably because you enjoy it was well. So what an excellent combination. You like it and you make  More impartial, objective, practical advice and insights to help with your property investing. We aim to help you improve your investment performance - increase returns & lower risks. A million visitors to our website a year take advantage of our insights – can a million people be wrong? – we doubt it.

More impartial, objective, practical advice and insights to help with your property investing. We aim to help you improve your investment performance - increase returns & lower risks. A million visitors to our website a year take advantage of our insights – can a million people be wrong? – we doubt it.  By property in Bratislava (30 miles from Vienna ) and or Tatry Mts in Slovakia – boom area (low tax, car factories providing new employment)

By property in Bratislava (30 miles from Vienna ) and or Tatry Mts in Slovakia – boom area (low tax, car factories providing new employment)

CPI inflation is still 2.8%, predicted to drop to about 2% by year end.

CPI inflation is still 2.8%, predicted to drop to about 2% by year end.  Our website has been predicting a

Our website has been predicting a

As the wealthy

As the wealthy  and investments are. A typical wealthy

and investments are. A typical wealthy  Most of these towns face south making them warmer than they normally would be because they catch the sun. The sea keeps them warm in the winter and cool in the summer. In west Cornwall, temperatures are normally 3 or 4 degrees C higher than the Midlands in February. So if you can find large Victorian apartments with sea views or any home with a sea view and good aspect, it will likely

Most of these towns face south making them warmer than they normally would be because they catch the sun. The sea keeps them warm in the winter and cool in the summer. In west Cornwall, temperatures are normally 3 or 4 degrees C higher than the Midlands in February. So if you can find large Victorian apartments with sea views or any home with a sea view and good aspect, it will likely  Some market analysis: just imagine you are a middle class baby-boomer living in London or the Midlands (the total population of this area is some 30 million people). You are now 50-60 years old. You have £200,000 of equity in your home. You are retiring in the next ten years. Where will you want to live – Birmingham, Croydon, Milton Keynes? No, however you will likely want to be within reach of your family, friends, and old business contacts and therefore you will

Some market analysis: just imagine you are a middle class baby-boomer living in London or the Midlands (the total population of this area is some 30 million people). You are now 50-60 years old. You have £200,000 of equity in your home. You are retiring in the next ten years. Where will you want to live – Birmingham, Croydon, Milton Keynes? No, however you will likely want to be within reach of your family, friends, and old business contacts and therefore you will  What we do know is there is very little building of new homes in Devon, Cornwall and the best coastal stretches of Dorset, Suffolk and Hampshire. So prices are almost certain to rise. It's simply supply and demand. And those doubting Thomas's that say "we'll all be moving abroad" – sorry, we just don't buy this. Reason – family, friends, part time employment and health care (and the TV, football and all the cultural aspects). Most of these retiring baby-boomers will end up putting up with the bad weather and traffic jams on the motorways – because they'll want to be close to their family and friends. So properties in

What we do know is there is very little building of new homes in Devon, Cornwall and the best coastal stretches of Dorset, Suffolk and Hampshire. So prices are almost certain to rise. It's simply supply and demand. And those doubting Thomas's that say "we'll all be moving abroad" – sorry, we just don't buy this. Reason – family, friends, part time employment and health care (and the TV, football and all the cultural aspects). Most of these retiring baby-boomers will end up putting up with the bad weather and traffic jams on the motorways – because they'll want to be close to their family and friends. So properties in  come at a discount in the current market. The best repossessions are properties that look tatty and superficially ugly (rubbish lying everywhere) but just need a good decoration to bring them back to normality. These properties might sell for £20,000 below similar well decorated properties, but only need a £2,000 tidy up and paint job. It's important to see through the mess and look at the fabric of the property – imagine what it would look like if properly decorated. I've yet to view a repossession that was not messy and needed re-decorating – and hence they normally sell for considerably less than normal properties.

come at a discount in the current market. The best repossessions are properties that look tatty and superficially ugly (rubbish lying everywhere) but just need a good decoration to bring them back to normality. These properties might sell for £20,000 below similar well decorated properties, but only need a £2,000 tidy up and paint job. It's important to see through the mess and look at the fabric of the property – imagine what it would look like if properly decorated. I've yet to view a repossession that was not messy and needed re-decorating – and hence they normally sell for considerably less than normal properties.  Gravesend-Ebbsfleet

Gravesend-Ebbsfleet  If you overlap all these development areas – it seems unlikely that places like Hackney Wick, Bow, Shoreditch , Canada Water,

If you overlap all these development areas – it seems unlikely that places like Hackney Wick, Bow, Shoreditch , Canada Water,  This zone started about ¼ miles south of the station. And remember, London Bridge is the site of the Glass Shard building planned to be

This zone started about ¼ miles south of the station. And remember, London Bridge is the site of the Glass Shard building planned to be  The Football World Cup is planned for mid 2010. There will be new stadiums built and big infra-structure improvements in Jo'burg, Cape Town and other cities. The confidence this event will bring to the country will be great and property prices will likely follow upwards in the lead up to 2010. Property prices have doubled in the last few years and are expected to moderate to about a 10% increase this year. However, as in all the most desirable global areas, some parts of South Africa are likely to beat the national average. Examples include:

The Football World Cup is planned for mid 2010. There will be new stadiums built and big infra-structure improvements in Jo'burg, Cape Town and other cities. The confidence this event will bring to the country will be great and property prices will likely follow upwards in the lead up to 2010. Property prices have doubled in the last few years and are expected to moderate to about a 10% increase this year. However, as in all the most desirable global areas, some parts of South Africa are likely to beat the national average. Examples include:  Cape Town - Camps Bay , Bantry Bay , Seapoint, Cliftonville, Llandudno, Hout Bay , Wynburg

Cape Town - Camps Bay , Bantry Bay , Seapoint, Cliftonville, Llandudno, Hout Bay , Wynburg  The outcome of the UK first super casino licence bid process was announced on Tuesday 31 st January - to everyone's surprise Manchester won the bid. It's likely the friction between the bids from Blackpool and London Greenwich had something to do with this - they both threatened the selection committee with legal action. Manchester has a large population within its catchment area and is a good regeneration location. Clearly it's come as very bad news for Blackpool and Greenwich. The area where the casino will be built - to the west of Manchester city centre close to the new Manchester City stadium - will undoubtedly experience a boost in property and land prices.

The outcome of the UK first super casino licence bid process was announced on Tuesday 31 st January - to everyone's surprise Manchester won the bid. It's likely the friction between the bids from Blackpool and London Greenwich had something to do with this - they both threatened the selection committee with legal action. Manchester has a large population within its catchment area and is a good regeneration location. Clearly it's come as very bad news for Blackpool and Greenwich. The area where the casino will be built - to the west of Manchester city centre close to the new Manchester City stadium - will undoubtedly experience a boost in property and land prices.  There is likely to be an immediate surge in house prices, though the jury is out on how much long term positive impact the super casino will have. There are likely to be 2700 new jobs and £275 million invested in the casino - but compared with the 30,000 jobs a year being created in London's financial centres, it is relatively small. It might help

There is likely to be an immediate surge in house prices, though the jury is out on how much long term positive impact the super casino will have. There are likely to be 2700 new jobs and £275 million invested in the casino - but compared with the 30,000 jobs a year being created in London's financial centres, it is relatively small. It might help  The

The  Globalization and the internet: have created great efficiency gains, cost reductions and reduced the pressure on inflation - India and China have helped enormously in providing cheap imports - manufacturing and distribution are now far more global with trade barriers dropping.

Globalization and the internet: have created great efficiency gains, cost reductions and reduced the pressure on inflation - India and China have helped enormously in providing cheap imports - manufacturing and distribution are now far more global with trade barriers dropping.  High earnings: In most developed countries, earnings growth is running well ahead of core inflation - in the UK, earnings growth in 2006 was 4.4%, whilst CPI inflation was 2% - taxes have risen, but not enough to dent consumer confidence.

High earnings: In most developed countries, earnings growth is running well ahead of core inflation - in the UK, earnings growth in 2006 was 4.4%, whilst CPI inflation was 2% - taxes have risen, but not enough to dent consumer confidence.  You have all this on the coast road from Cape Town through to Sea Point, Cliftonville, Bantry Bay, Camps Bay, Llandudno to Hout Bay. Camps Bay - Bantry Bay are the closest you will get to the St Tropez of Africa - the best beach front penthouses now sell for £1 million. Cape Town harbour is rapidly developing with nice marina, shops and restaurants - and good maritime history. The St Clements area suburb of Cape Town has big executive houses with good security - these make popular long term corporate rentals. Most living costs are half what they are in the UK - no sign of this changing. Hout Bay is a more family oriented alternative residential area and is definitely up and coming - some new select gated developments are being built, the town does have a growing Township of squatters. Further south along the dramatic coastline is Hoek Bay - a rather Bohemian place frequented by surfers - definitely up and coming. Likely to become more mainstream and popular in the next ten years.

You have all this on the coast road from Cape Town through to Sea Point, Cliftonville, Bantry Bay, Camps Bay, Llandudno to Hout Bay. Camps Bay - Bantry Bay are the closest you will get to the St Tropez of Africa - the best beach front penthouses now sell for £1 million. Cape Town harbour is rapidly developing with nice marina, shops and restaurants - and good maritime history. The St Clements area suburb of Cape Town has big executive houses with good security - these make popular long term corporate rentals. Most living costs are half what they are in the UK - no sign of this changing. Hout Bay is a more family oriented alternative residential area and is definitely up and coming - some new select gated developments are being built, the town does have a growing Township of squatters. Further south along the dramatic coastline is Hoek Bay - a rather Bohemian place frequented by surfers - definitely up and coming. Likely to become more mainstream and popular in the next ten years.  The economics of South Africa are less compelling - GDP growth of 3% is not stellar by any means. The Rand has dropped from 10 to 14 to the pound - this despite metal prices booming. It's still difficult to take Rand out of the country. Commissions on property sales are high - like in Spain. Manufacturing centred in Johannesburg is doing well, but they have to compete with India and China, so the longer term outlook may not be so good. The crime problems don't seem to be getting any better. So South Africa is not without its risks though any property investor visiting Cape Town and seeing Table Mountain, the Seven Apostles and all the beautiful beaches, wildlife, wineries, sun, sand, sea, scenery and culture will feel like buying a property.

The economics of South Africa are less compelling - GDP growth of 3% is not stellar by any means. The Rand has dropped from 10 to 14 to the pound - this despite metal prices booming. It's still difficult to take Rand out of the country. Commissions on property sales are high - like in Spain. Manufacturing centred in Johannesburg is doing well, but they have to compete with India and China, so the longer term outlook may not be so good. The crime problems don't seem to be getting any better. So South Africa is not without its risks though any property investor visiting Cape Town and seeing Table Mountain, the Seven Apostles and all the beautiful beaches, wildlife, wineries, sun, sand, sea, scenery and culture will feel like buying a property.  Most Buy-to-Let investors never intended to become professional Landlords - they only got

Most Buy-to-Let investors never intended to become professional Landlords - they only got  If you want an easier life, you might consider selling up and

If you want an easier life, you might consider selling up and  We know of someone who became a millionaire from spotting a steep plot on the side of a road in Cornwall - it was completely overlooked - but he managed to get planning permission for a block of flats - the plot looked out over the sea - a developer bought it from him. He made a 1000% return on investment.

We know of someone who became a millionaire from spotting a steep plot on the side of a road in Cornwall - it was completely overlooked - but he managed to get planning permission for a block of flats - the plot looked out over the sea - a developer bought it from him. He made a 1000% return on investment.  The key thing about land is - spotting an opportunity preferably one that no one else has spotted - and when you have spotted it - securing an option on it. Many land deals break down because the land owner either distrusts the purchaser or likes the idea of selling it then goes to someone else for a higher price or better terms. Land is a very emotional asset - many land owners have had land in their family for years - they like to stay in control and do not like to lose control during the deal making process. So how you relate to the land owner is particularly important. We suggest you give references to prove you are trustworthy - if you are acting for a company, this may help. If it's a well known land company, even better. But land deals are also open to individuals - and you'll have to try and learn as you go how best to treat each land owner.

The key thing about land is - spotting an opportunity preferably one that no one else has spotted - and when you have spotted it - securing an option on it. Many land deals break down because the land owner either distrusts the purchaser or likes the idea of selling it then goes to someone else for a higher price or better terms. Land is a very emotional asset - many land owners have had land in their family for years - they like to stay in control and do not like to lose control during the deal making process. So how you relate to the land owner is particularly important. We suggest you give references to prove you are trustworthy - if you are acting for a company, this may help. If it's a well known land company, even better. But land deals are also open to individuals - and you'll have to try and learn as you go how best to treat each land owner.  Some will want to spend lots of time building a relationship before doing a deal - others will work faster but may take their impression on their first encounter with you. It's a tough business line - but the rewards are tremendous. It will take much time, scouting for land, knocking on doors, having meetings, persuading owners why they should sell to you. You might scout and identify 1000 plots of land, approach 100 owners and get a meeting with 5 of them. Only two might lead to options on a plot of land and one to an actual sale. If you like certainty and not being rejected, it will not be for you. If you like to follow a system, like making cold calls, investigating ownership, are highly motivated and do not mind being told to walk, it could be just the business. It's possible to do the job whilst working full time, but visiting people during normal office hours is most common - so you might struggle if you have a full time job.

Some will want to spend lots of time building a relationship before doing a deal - others will work faster but may take their impression on their first encounter with you. It's a tough business line - but the rewards are tremendous. It will take much time, scouting for land, knocking on doors, having meetings, persuading owners why they should sell to you. You might scout and identify 1000 plots of land, approach 100 owners and get a meeting with 5 of them. Only two might lead to options on a plot of land and one to an actual sale. If you like certainty and not being rejected, it will not be for you. If you like to follow a system, like making cold calls, investigating ownership, are highly motivated and do not mind being told to walk, it could be just the business. It's possible to do the job whilst working full time, but visiting people during normal office hours is most common - so you might struggle if you have a full time job.  Be aware, any piece if land is a potential value creating opportunity. If you envisage you can purchase at below market value, quickly add value (e.g. by gaining planning permission), and the plot is marketable, then you will make the biggest profit. Don't expect to make any money buying a remote piece of Scottish Highland. But if you buy a 2 acre agricultural plot next to an intersection on the M25, then get planning permission for commercial development, you might make £2 million in six months. If you buy a ½ acre plot in SE England for £20,000 without planning permission, then gain planning permission for a 4 bedroom detached executive house, the land will be worth around £180,000 - a £160,000 gain in six months.

Be aware, any piece if land is a potential value creating opportunity. If you envisage you can purchase at below market value, quickly add value (e.g. by gaining planning permission), and the plot is marketable, then you will make the biggest profit. Don't expect to make any money buying a remote piece of Scottish Highland. But if you buy a 2 acre agricultural plot next to an intersection on the M25, then get planning permission for commercial development, you might make £2 million in six months. If you buy a ½ acre plot in SE England for £20,000 without planning permission, then gain planning permission for a 4 bedroom detached executive house, the land will be worth around £180,000 - a £160,000 gain in six months.  Prices have risen up to 25% since the Olympics was announced in July 2005 in

Prices have risen up to 25% since the Olympics was announced in July 2005 in  why prices are slow to rise. Take a look at Hackney Wick - this is a beautiful Victorian area with a village feel with excellent road communication and only 2/3 of a mile to the new Stratford International station. The southern fringes of Leytonstone and Wanstead Flats have some nice big Victorian houses - which will be very popular in years to come with West Londoners who settle in the East after improvements in communications and after the Olympic park is built - some £5 billion of investment is expected, along with £2 billion on the retail and office complex around the next Stratford International Station.

why prices are slow to rise. Take a look at Hackney Wick - this is a beautiful Victorian area with a village feel with excellent road communication and only 2/3 of a mile to the new Stratford International station. The southern fringes of Leytonstone and Wanstead Flats have some nice big Victorian houses - which will be very popular in years to come with West Londoners who settle in the East after improvements in communications and after the Olympic park is built - some £5 billion of investment is expected, along with £2 billion on the retail and office complex around the next Stratford International Station.  Other areas which will do well are Bow - equidistant from Stratford, Docklands and the City. Limehouse basin - the upmarket marina area half way between the Canary Wharf and the City will also benefit. Canning Town and Silvertown, two rather bleak 1960s housing estates have excellent communications and crime levels are dropping - worth considering for higher yield higher risk property investment. Plaistow and West Ham are also close to Stratford, they are cheaper and most areas are a bit down-at-heel but regeneration has been taking place for years - the areas will benefit from close proximity to the Olympic Park down the Lower Lees Valley and from being only 1½ miles from Stratford International Station.

Other areas which will do well are Bow - equidistant from Stratford, Docklands and the City. Limehouse basin - the upmarket marina area half way between the Canary Wharf and the City will also benefit. Canning Town and Silvertown, two rather bleak 1960s housing estates have excellent communications and crime levels are dropping - worth considering for higher yield higher risk property investment. Plaistow and West Ham are also close to Stratford, they are cheaper and most areas are a bit down-at-heel but regeneration has been taking place for years - the areas will benefit from close proximity to the Olympic Park down the Lower Lees Valley and from being only 1½ miles from Stratford International Station.  Other areas worth considering are Woolwich which will shortly get an extension to the Docklands Light Railway and New Cross Gate, Peckham, Brockley and Syndenham which will almost certainly get a new tube service by about 2011 - the long awaited East London Line extension - which will whisk commuters to Wimbledon, Croydon and Hackney via the City. A new station is planned at the intersection on Surrey Canal Road (next to the incinerator) just north of New Cross Gate.

Other areas worth considering are Woolwich which will shortly get an extension to the Docklands Light Railway and New Cross Gate, Peckham, Brockley and Syndenham which will almost certainly get a new tube service by about 2011 - the long awaited East London Line extension - which will whisk commuters to Wimbledon, Croydon and Hackney via the City. A new station is planned at the intersection on Surrey Canal Road (next to the incinerator) just north of New Cross Gate.  But GDP growth is still a healthy at 3% and although inflation is rather higher than Bernacker would like, it seems to be fairly well under control. It looks like the USA may be close to the top of its interest rate cycle - the dollar will likely decline further against the Euro and Yen, particularly if rates drop soon. The USA is no longer the global growth engine - this mantle has passed to China. It's still the most important economy in the world, but

But GDP growth is still a healthy at 3% and although inflation is rather higher than Bernacker would like, it seems to be fairly well under control. It looks like the USA may be close to the top of its interest rate cycle - the dollar will likely decline further against the Euro and Yen, particularly if rates drop soon. The USA is no longer the global growth engine - this mantle has passed to China. It's still the most important economy in the world, but  For the international property investor, it's now more difficult to see value in property investment in the USA. One can envisage prices staying flat or rising slowly, but with the dollar falling against the Euro and Sterling. Coastal areas of the western Florida pan-handle still look good value - they also tend to avoid the worst of the hurricanes.

For the international property investor, it's now more difficult to see value in property investment in the USA. One can envisage prices staying flat or rising slowly, but with the dollar falling against the Euro and Sterling. Coastal areas of the western Florida pan-handle still look good value - they also tend to avoid the worst of the hurricanes.  The rapid population growth in Florida, shortage of land and increasing environmental constraints along with all those retiring babyboomers from NE USA will likely lead to higher prices in Florida in the coming years. Increasing tourism will also help cities like Orlando and Miami particularly if there are no big punitive taxes on flying (ref: climate change).

The rapid population growth in Florida, shortage of land and increasing environmental constraints along with all those retiring babyboomers from NE USA will likely lead to higher prices in Florida in the coming years. Increasing tourism will also help cities like Orlando and Miami particularly if there are no big punitive taxes on flying (ref: climate change).