UK Market Update

Nationwide reported prices dropping by 1.2% in July. Similar trends were report by Halifax and Hometrack (-1.2%). Rightmove reported a mixed bag, with some parts of London still rising (London rose +0.3% overall). The Land Registry numbers were a little more positive, though these figures are about 4 weeks behind the other indications (note: Rightmove has the leading indicator).

Nationwide reported prices dropping by 1.2% in July. Similar trends were report by Halifax and Hometrack (-1.2%). Rightmove reported a mixed bag, with some parts of London still rising (London rose +0.3% overall). The Land Registry numbers were a little more positive, though these figures are about 4 weeks behind the other indications (note: Rightmove has the leading indicator).

Clearly the UK market slowdown continues with property prices falling in almost all areas because of a combination of:

• Credit squeeze – banks are reluctant to lend high multiples of income, and are demanding high deposits to reduce their risk of default and negative equity

• GDP slowdown - the economy is growing at ca. 1.5% per annum, and may be heading for a couple of quarters of recession, hence consumer confidence is low, unemployment is rising slightly and wage growth has moderated to ca. 3.5% per annum (from 4.0 to 4.4% in 2007)

• Buy to let investors are buying less – likely waiting for prices to drop further and more bargains to appear

• First time buyers – have dropped to a half of levels three years ago – they are almost non existent

• Existing homeowners – the introduction of home information packs, high stamp duty taxes and moving costs has meant many existing owners have chosen to stay put and instead extend their homes. Difficulties getting kids into good schools means many owners, once they have got established in work and schooling arrangements, are reluctant to risk moving

• Existing homeowners – the introduction of home information packs, high stamp duty taxes and moving costs has meant many existing owners have chosen to stay put and instead extend their homes. Difficulties getting kids into good schools means many owners, once they have got established in work and schooling arrangements, are reluctant to risk moving

• Taxes – the rises in stamp duty over the last ten years make it far less attractive for people to move home, particularly in southern England

• Debit – levels of debit got so high leading up to mid 2007 - many home owners and investors have now retrenched

• Inflation - the rise in CPI inflation from 1.5% a few years ago to the current 3.2% (driven in large part by higher oil prices between $125 to $145/bbl) has meant interest rates have remained at 5% making borrowing relatively expensive compared to the USA (2% base rate) and European mainland (4%).

• Developers – have been reducing prices of new build apartments to offload stock as balance sheets have deteriorated and many home builders have got into trouble with high levels of debit and dropping stock market valuations

• Manufacturing – is in recession, albeit a weakening pound should help exports later in 2008

• Young buyers – many young people prefer to rent rather than being saddled with huge mortgages, particularly now that most students leave college with massive student debits. They also like to travel, enjoy life and have families later in life – so deferring the purchase of a home is considered by many as an attractive option. Young immigrants also find it difficult raising finance in the UK and therefore rent instead.

The more positive underlying trends are:

• Rising population – an additional 5 million people will need homes in the next 20 years

• Rising population – an additional 5 million people will need homes in the next 20 years

• Stock market performance – the FT100 and other stock markets have not performed well and there continues to be interest in property as an alterative investment

• Oil prices – the UK benefits from high oil prices in taxes from the North Sea, oil/gas income and government taxes on oil/gas income from around the world that ends up in London and Aberdeen. Remember the UK is almost self sufficient in oil, and its gas imports are not high compared to most European countries

• Taxes – the government will likely go slow on tax increases moving forwards because the population cannot afford any more

• Smaller households – high divorce rates, partners owning two properties and an aging population of single people will mean more homes will be required in the next 20 years

• Inflation - with oil prices dropping to $125/bbl and the UK and global economies slowing, it may be possible for interest rates to drop in the second half of 2008 to 4.75% or even 4.5%

• Employment – levels remain high and unemployment is not likely to rise a significant extent in southern England and London

• Building – levels of home building are at such a low level that demand will eventually exceed supply and start supporting prices, possible late 2009 onwards. 240,000 new homes are required a year, but only a net 140,000 are being built (25,000 are demolished)

• Olympics and London Infra-structure – new investments, infra-structure and public spending in London in the run up to the 2012 Olympics will help support prices in London. £1.5 Bln retail park at White City and £1.5 Bln retail park at Stratford will also help.

• Olympics and London Infra-structure – new investments, infra-structure and public spending in London in the run up to the 2012 Olympics will help support prices in London. £1.5 Bln retail park at White City and £1.5 Bln retail park at Stratford will also help.

• Rental market – young people and immigrant workers have a preference or a necessity to rent – this should stimulate strong rental demand – rents are increasing – this should continue

We believe house prices will continue dropping for at least another 6 months. After this, depending on interest rates (and inflation, and oil prices) it's quite likely the market will stabilize. Interest spread rates are coming down and the main credit squeeze is starting to subside. It's too early to say when the drops will stop – or whether there will be a prolonged downturn. Much depends on consumer confidence, and the government's management of the economy and whether the UK slips into recession and job losses accelerate. All these are quite uncertain.

Clearly for the first time buyer or new property investor it will be a high risk period. For seasoned property investors who are cash rich, opportunities abound, and these could increase towards the end of 2008.

To reduce investment risk, it's worth considering purchasing property only in developing city areas – and London probably provides the best opportunities and lowest risk of a fully fledged property price crash. The reason is levels of borrowing as a proportion of property value remain relatively low in London as wages are higher. As long as the financial sector does not contract, the sheer scale of wealth in the city and foreign investment in property and business should support prices. This is evidenced by the “ super-prime” property prices in Kensington and Chelsea still being on the rise in July. The trick is to find bargains in areas that are regenerating close to very expensive areas – these should experience a ripple effect up until the Olympics of 2012. This is the reason why we have prepared an infra-structure review of London outlined below, to help you with your investment insights and decisions.

To reduce investment risk, it's worth considering purchasing property only in developing city areas – and London probably provides the best opportunities and lowest risk of a fully fledged property price crash. The reason is levels of borrowing as a proportion of property value remain relatively low in London as wages are higher. As long as the financial sector does not contract, the sheer scale of wealth in the city and foreign investment in property and business should support prices. This is evidenced by the “ super-prime” property prices in Kensington and Chelsea still being on the rise in July. The trick is to find bargains in areas that are regenerating close to very expensive areas – these should experience a ripple effect up until the Olympics of 2012. This is the reason why we have prepared an infra-structure review of London outlined below, to help you with your investment insights and decisions.

Outside London, areas with a projected strong employment prospects are also attractive – some examples are:

- Aberdeen (oil companies, BP, Shell)

Cambridge St Neots (high tech jobs)

Cambridge St Neots (high tech jobs) - Reading (British Gas)

- White City-London (2008, 7000 new jobs, £1.6 Bln retail development)

- Stratford-London (2012, 7000+ new jobs, retail development)

- Newbury (Vodaphone)

- Southampton (new business)

- Kettering (transport hub, new businesses)

- Exeter (met office jobs, new business)

Historic cities and market towns with good schools and universities should continue to experience better house price stability during a downturn – examples are:

Oxford

Oxford - Cambridge

- Warwick

- York

- Harrogate

- Lancaster

- Stratford on Avon

- Bath

- Exeter

- Taunton

- Skipton

London regeneration and infra-structure update for property investors

For all the serious London property investors, we have prepared a summary of the key infra-structure upgrades, mainly in East London, that we believe will impact asset prices and returns in future. Beyond any doubt, a new rail or tube station helps with bringing new wealth, income, jobs and prosperity into an area - helps deprived areas and increases rental demand and property demand generally. It's not rocket science. We have systematically researched the latest timings and stations to be built, to help you in your investment decisions.

A. Dockland Light Railway Extensions

Any property close to these new stations will see their value increase relative to the average London property. We have summarised the branch extensions - with new stations and timing:

1. Woolwich Arsenal 2009 (from Silvertown via North Woolwich via new tunnel under Thames)

2. Stratford 6 km extension – 2010

3. Langdon Park (north of All Saints near Bow) new station on old line under construction

4. Dagenham Extension – proposal ony - possibly 2012

- Beckton Riverside would serve the development proposals for the area between the River Thames and the A1020 in the vicinity of the proposed Thames Gateway Bridge.

- Creekmouth, Barking Riverside and Goresbrook (formerly Dagenham Vale) stations would be located so as to maximise catchments within the Barking Riverside development.

- Dagenham Dock station would be an interchange

These light rail developments link to Stratford - the main site for the London Olympics of 2012. These areas will likely encounter faster regeneration because of the new communications. Some of these areas will be transformed. Woolwich is a good example - one will be able to travel via DHL to Canary Wharf (20 minutes!) then Bank in the City of London (27 mins) without changing - and this is sure to boost prosperity and with it property prices. At present, it takes about 50 minutes to get to Bank - so now Woolwich will be open to all the city workers who earn high salaries and want to live along the Thames in a regenerating area up-river. Okay, we all know Woolwich is not Battersea, but it will certainly show improvement over time because of this new infra-structure development. And anyone that has ever visited wind swept North Woolwich in the winter will know this new development cannot have come quick enough.

These light rail developments link to Stratford - the main site for the London Olympics of 2012. These areas will likely encounter faster regeneration because of the new communications. Some of these areas will be transformed. Woolwich is a good example - one will be able to travel via DHL to Canary Wharf (20 minutes!) then Bank in the City of London (27 mins) without changing - and this is sure to boost prosperity and with it property prices. At present, it takes about 50 minutes to get to Bank - so now Woolwich will be open to all the city workers who earn high salaries and want to live along the Thames in a regenerating area up-river. Okay, we all know Woolwich is not Battersea, but it will certainly show improvement over time because of this new infra-structure development. And anyone that has ever visited wind swept North Woolwich in the winter will know this new development cannot have come quick enough.

Watch out also for the Dagenham development which may or may not proceed - a direct link between Canary Wharf and Dagenham would undoubtedly have a big positive impact on the area.

Watch out also for the Dagenham development which may or may not proceed - a direct link between Canary Wharf and Dagenham would undoubtedly have a big positive impact on the area.

B. East London Line Extension

Here we summarize the latest timing and stations to be built on the "East London Line tube extension". Many of these areas will be transformed particularly those that currently have no station and are also far from an existing railway station - Haggerston is probably the best example. By 2009, we'll be able to travel by tube from Highbury to New Cross Gate without changing train. It will open up New Cross Gate and New Cross to the vibrant City and north of London - very exciting.

2009 New tube trains

- Dalston Junction

- Haggerston

- Hoxton

- Shoreditch High St

- Through trains to New Cross Gate (terminating)

2010 East London Railway Opens - through trains to:

- New Cross Gate (already open, now a through station to West Croydon)

- Honor Oak Park

Forest Hill Sydenham

Forest Hill Sydenham - Crystal Palace

- Penge West

- Anerley

- Norwood Junction

- West Croydon

Phase 2 (to be announced)

- Surrey Canal Road

- Queens Rd Peckham

- Peckham Rye

- To Wimbledon (possibly via Clapham Junction)

- Brockley

In 2010, the above-mentioned stations will open - transforming places like sleepy Brockley and Honor Oak into the mainstream tube world. Large tracks of SE London Victoriana will become accessible to City workers - we expect this to positively impact property prices.

Workers will be able to travel from Highbury all the way to West Croydon by tube - overland on "East London Railway" from New Cross Gate southwards. We've been waiting years for this exciting development and this extension to West Croydon is now 95% certain of happening.

Phase 2 seems to be suffering a bit of delay - this is the section from a new station called "Surrey Canal Road" near Millwall Football Ground (next to the Incinerator) via Queens Rd Peckham, Peckham Rye all the way to Wimbledon. We'll keep you posted on any developments here - it's likely to happen though, but possibly not until 2012 or later.

Any residential property investment within 3-5 minutes walk of these new stations will see a big benefit in both rental demand and asset prices after station completion. We hope you have found this research helpful in assisting London property investors.

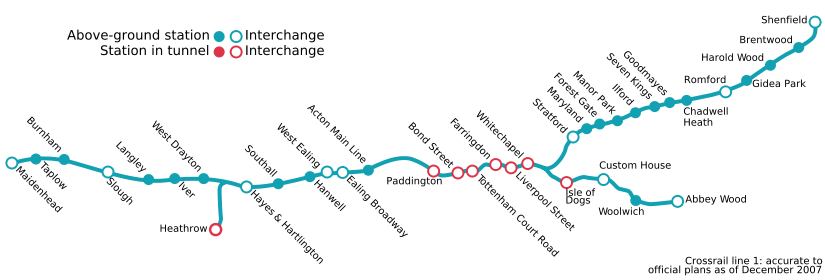

C. Crossrail – a massive £16 Bln new project

This huge project got the go ahead in July. At peak times, 24 trains per hour will run in each direction through central London and reach speeds of up to 100 mph on open stretches and 60mph in the tunnels. Heathrow will be 31 minutes away from the West End and 43 minutes from Canary Wharf.

New stations are planned at Paddington, Bond Street, Tottenham Court Road, Farringdon, Whitechapel, Liverpool Street and Isle of Dogs. The heart of Crossrail with interchanges in all directions will be Farringdon – a one bedroom flat close to this station will surely be a good long term investment. Relatively down at heel Tottenham Court Road will get a boost. Liverpool Street will see a boost, and benefit also from the East London Line extension and proximity to Eurostar at Kings Cross. Lots of good news for these central areas.

Crossrail will link the West End with Southall (19 mins), Woolwich (22 mins), Ilford (20 mins) and Romford (31 mins). Likely completion date is 2014 if all goes to plan. Expect further price rises in these suburbs as the West End and City opens up to these previously deprived areas.

Abbey Wood will be a big beneficiary – this place is almost impossible to reach at present. It will have direct access to City jobs and the West End. Prices should rise dramatically if and when the project is complete. Let's hope the project goes through the execution phase. It's been 20 years in discussion and the city will see huge benefits in previously deprived areas because of this project.

UK property hotspots 2008 for a 2-3 year timeframe

We often have requests for our Property Hotspots listing – we enclose the listing for 2008. It's important to note that for most of these areas, we do not expect prices to rise this year. There may be the odd exception – some parts of London may still see small rises such as Soho and Islington. And in the “super-prime” market frequented by wealthy people from Middle East, Russia, Africa, USA, South Asia and the Far East – prices could well continue to rise – such areas include Mayfair, Chelsea, Kensington, Knightsbridge and Notting Hill.

The main objective of presenting this list though is to allow interested investors who have cash and funding to seek out the best opportunities in a 1-3 year time frame. It's quite possible prices may start rising by mid 2009 in these areas if interest rates drop late 2008 and oil prices stay at or below $125/bbl – we do not know when property prices in the UK will bottom out or how severe the downturn will turn out to be. Some areas like Oxford have not experienced any downturn as yet – primarily because of people wanting to move to the City because of its education, history, surroundings and expanding businesses.

The main objective of presenting this list though is to allow interested investors who have cash and funding to seek out the best opportunities in a 1-3 year time frame. It's quite possible prices may start rising by mid 2009 in these areas if interest rates drop late 2008 and oil prices stay at or below $125/bbl – we do not know when property prices in the UK will bottom out or how severe the downturn will turn out to be. Some areas like Oxford have not experienced any downturn as yet – primarily because of people wanting to move to the City because of its education, history, surroundings and expanding businesses.

The listing is very selective. You will notice no hotspots in the Midland, East Midlands and many northern areas. The closest to a hotspot we would venture in East Midlands is Doncaster, because of its fast train link to London. In the Midlands, we'd go as far south as Gloucester, Tewksbury, Cotswolds and Cheltenham before picking up any area we believe to be more secure from the downturn. Many areas of Manchester may see prices staying firm because of the strong business in this major city. But overall, the drop in public spending growth, manufacturing being clobbered and lower incomes in the north we believe will have a pretty severe impact on property prices in the next year.

Areas in the listing have been selected because of a number of positive factors that will support prices and lead to increases in future years:

- Regeneration

- Improvements in communications – rail, tube, road, bridge, tunnel

- Olympics

- Jobs market exposed to international wealth and finance

- Ripple effect from more expensive neighbouring areas

- Retiring babyboomers, holiday homes and second homes

- Shortage of land, shortage of supply, increasing population

- Education, universities, knowledge

- Oil wealth

With the Olympics coming up in 2012, it's hard to believe that places like Hackney Wick, south Hackney, Stratford and Bow will not see prices rising. With Ebbsfleet arriving, it's difficult to see how Gravesend will not see prices rise in a 2 year time frame – especially when the fast commuter trains start in 2010. Dartford, Rochester, Northfleet, Strood, Southfleet and Istead Rise will all be positively impacted.

Table: 2008 UK Hot Spots - PropertyInvesting.net - 3 year view

| London | Reasons | Rating |

| Soho, Bloomsbury | Midway West End/Mayfair and City - massive wealth, nightlife | 9 |

| West Kensington | Spill over from Kensington - huge wealth/finance | 8.5 |

| Lambeth - South Bank | Proximity to West End, mid-town, City and Docklands | 8.5 |

| London Bridge - Old Kent Rd | Proximity to City, stations, night-life | 8.5 |

| Peckham (Queens Rd) | East London tube station promised, distant Olympic effect | 8 |

| Kennington | Gentrification, proximity to Westminster | 7 |

| Hackney - Hoxton | Gentrification, Olympic effect, proximity to City & Stratford | 7 |

| Elephant & Castle | Proximity to City, West End, regeneration | 7 |

| Chelsea | Wealthy international investors, city bonuses | 7 |

| Bow - Bow Church - Shoreditch | Olympics, proximity to City, Stratford, regeneration | 7 |

| Bayswater | Proximity to West End, Notting Hill, Hyde Park - good value | 7 |

| Battersea | Gentrification, proximity to Chelsea | 7 |

| New Cross Gate - Telegraph Hill | E London line tube extension, regeneration, proximity to City | 7 |

| Woolwich | DHL extension due by ca. 2010, cheap, regeneration | 6 |

| White City - Shepherds Bush | Retail development, regeneration proximity to West End | 6 |

| Stratford - Plaistow | Olympics, new Eurostar station, regeneration, retail | 6 |

| Royal Docks, Silvertown, N Woolwich | New DHL extension, city jobs, Olympic affect | 6 |

| Limehouse | Midway Docklands and City - jobs | 6 |

| Forest Hill - Catford | East London Line extension opening late 2007 | 6 |

| Clapham | Gentrification, proximity to West End, City | 6 |

| Canada Water | Regeneration of £1 billion, one stop to Canary Wharf | 5 |

| | | |

| South East | | |

| Gravesend - Northfleet - Southfleet | New Eurostar station at Ebbsfleet | 8 |

| Cambridge | Top education, history, promixity to London, house shortage | 6 |

| Ramsgate | Fast commute to Kings Cross in 2009, nice harbour | 6 |

| Newbury | Shortage of homes, big business, A14 improvement | 6 |

| Reading | Oil company HQ, M4 corridor, close to Heathrow and London | 6 |

| Winchester | Excellent education, history, shortage of homes, wealth | 6 |

| Oxford | Top education, history, promixity to London, house shortage | 6 |

| Rochester-Strood | Regeneration, proximity to Ebbsfleet | 6 |

| | | |

| S Midlands | | |

| St Neots | High-tech business, close to Cambridge, A14 improvement | 7 |

| | | |

| North, North West | | |

| Bury | Regeneration from low base - for 5 year outlook only | 6 |

| Skinningrove | Late regeneration and identified as nice seaside village | 5 |

| Bradford | Regenaration from low base - price could rise late 2009 | 5 |

| | | |

| South West | | |

| Portreath | Regeneration, airport, beaches | 8 |

| Hayle | On A30, rail, big harbour development, close to St Ives | 8 |

| Newquay | Regeneration, proximity to Padstow and Truro, airport, A30 | 7 |

| St Just | Regeneration, Heritage Site | 7 |

| Weymouth | Olympics and regeneration | 7 |

| Swanage | Proximity to Sandbanks - late regeneration | 6 |

| | | |

| Wales | | |

| Barry Island | Spill over coastal resort near Cardiff | 5 |

| | | |

| Scotland | | |

| Aberdeen, Stonehaven | Oil boom, catch up since mid 1980s | 9 |

| Dundee | Low prices, regenerating, nice countryside | 8 |

If you can use the quiet market and relatively high interest rates to seize on opportunities, it might do you good in future years. Not without its risks of course, but we believe focusing on these areas – particularly where new jobs are being created – will help your investment returns in a 2-3 year time frame.

Woolwich is an interesting example – depressed, down at heel, high unemployment, south of the river – many things going against it. But with the Docklands Light Railway Extension due to open in 2009, Olympics 4 miles away, city jobs close by and a low price base – it's an area that will improve substantially in the next ten years. Expect prices to drop for the next year as some distressed sellers come into the market. It will improve in the longer term though. The larger Victorian properties towards Plumstead are also worth considering. Crime is relatively high at present, but as the area improves, this should reduce.

Woolwich is an interesting example – depressed, down at heel, high unemployment, south of the river – many things going against it. But with the Docklands Light Railway Extension due to open in 2009, Olympics 4 miles away, city jobs close by and a low price base – it's an area that will improve substantially in the next ten years. Expect prices to drop for the next year as some distressed sellers come into the market. It will improve in the longer term though. The larger Victorian properties towards Plumstead are also worth considering. Crime is relatively high at present, but as the area improves, this should reduce.

Closer to the city, a safer bet is New Cross Gate - Nunhead - Peckham. This area will benefit from the East London Line Extension from 2009 – 2010. A new station at Surrey Canal Road should eventually transform this part of London near Millwall football ground. The Hatcham Park conservation area close by is already popular - though it's likely to become more so in the future.

In the north of the UK, as we have been mentioning for 18 months now, Aberdeen is a hotspot. A shortage of land, property and building, employment growth in the oil/gas sector and wealthy retiring oil workers all play in its favour. The corporate lettings market is vibrant. City centre apartments and nice old detached properties in central areas are probably the best opportunities. Stonehaven and Dundee are both experiencing positive spillover from Aberdeen. Anywhere within 40 miles of Aberdeen is worth considering, unless you think the oil price will crash.

Overseas European Investment

We believe the European economy will take a knocking in the next few years as interest rates rise, inflation stays stubbornly high (because of oil prices at $125+/bbl) and the general tough banking conditions in the western economies. Exports to the Far East are helping, but the Euro seems overvalued – probably by about 20% against fundamentals. We expect the Euro to decline along with the UK Sterling in the next year. This should help exports and growth but property asset values on a US $ or global basis will suffer because of it.

We have ranked the countries we believe will see highest house price growth (top) with those showing falls (bottom). The general trend is that the newly joined up Euro countries will see prices rising, with the older ones seeing stagnant or falling prices. Italy will suffer from high oil/gas import costs, as will Spain and Greece. Less airline travel to these holiday destinations because of higher airline fuel prices will also dent demand for property in these countries. An exception is Cyprus with an influx of Middle Eastern money and tourism helping the small economy of this Island.

We have ranked the countries we believe will see highest house price growth (top) with those showing falls (bottom). The general trend is that the newly joined up Euro countries will see prices rising, with the older ones seeing stagnant or falling prices. Italy will suffer from high oil/gas import costs, as will Spain and Greece. Less airline travel to these holiday destinations because of higher airline fuel prices will also dent demand for property in these countries. An exception is Cyprus with an influx of Middle Eastern money and tourism helping the small economy of this Island.

The list is ranked in terms of certainty of house price rises (top) to house price drops (bottom) in the next two years:

- Russia

- Norway

- Cyprus

- Albania

- Romania

- Montenegro

- Serbia

- Poland

- Luxembourg

- Hungary

- Malta

- Croatia

- Belgium

- Finland

- Solvenia

- Slovakia

- Bulgaria

- Denmark

Lithuania

Lithuania - Czech Republic

- Switzerland

- Sweden

- Holland

- Austria

- Turkey

- Latvia

- Germany

- Estonia

- UK

- Ireland

- Spain

- Italy

- Iceland

The countries with the biggest potential upside in house prices movements are probably:

- Albania

- Romania

- Poland

- Montenegro

-

Albeit some of these countries or regions are also high risk, particularly Albania. Probably the lowest risk but biggest upside country is Romania – with regenerating second hand property in Bucharest the capital being the highlight, particularly in the more prosperous central suburbs. As wealthy Romanians return home from foreign working missions, they will want high class apartments and houses close to the city centre in the better areas of the city (north and north-western central suburbs).

Krakow and Warsaw in Poland are also likely to be hotspots – prices will benefit from the proximity to Germany and Russia – its wealthy near neighbours.

For the safest haven, Norway is beyond doubt secure, wealthy, with massive oil/gas income and beautiful scenery (when it's not raining). With small population and environmental restrictions, expect property prices to continue rising on an ongoing steady basis. Oil towns of Stavanger and Bergen should do well, with Oslo following behind.

Every country has a different market, and asset prices of certain properties will perform better than others. The three key categories one can split property into are:

- Residential : Apartments and houses, in cities, towns, villages, and isolated rural areas - principle homes, holiday homes (private or let)

- Commercial : Warehouses, factories, retail shops

- Land : farmland, residential building land, commercial land, forestry/other

In emerging economies with rapid GDP growth, normally the prosperous cities are the areas which have strongest property price growth over time. This is where jobs are created and wealth is focused. Land restrictions and demand drive prices up. Holiday homes and second homes in countryside or seaside areas also tend to follow. Central city land prices will rise the first, then ripple out to country areas close to the cities. So, as a general rule, for residential property investors – if you purchase historic city centre apartments and houses in regenerating suburbs close to prosperous city centres in the capitals or second cities, you are likely to see prices rising sharply. An example was Prague though this is now quite a mature market. Newer examples are Warsaw (Poland), Bucharest (Romania), Sofia (Bulgaria), Krakow (Poland) and Bratislava (Slovakia), Tirana (Albania) and Ljubljana (Solvenia).

Concluding Remarks: We hope you are enjoying your property investing so far in 2008 – more challenging times than most, but with lots of opportunities.