More impartial, objective, practical advice and insights to help with your property investing. We aim to help you improve your investment performance - increase returns & lower risks. A million visitors to our website a year take advantage of our insights – can a million people be wrong? – we doubt it.

More impartial, objective, practical advice and insights to help with your property investing. We aim to help you improve your investment performance - increase returns & lower risks. A million visitors to our website a year take advantage of our insights – can a million people be wrong? – we doubt it.

Ideas

PropertyInvesting.net are pleased to provide a list of property ideas – these have been compiled over the last 3 years. We hope they stimulate some good thoughts for your own investment plans. You might choose to rank them using your own criteria – to screen out the ones you are not so keen on. We hope you find these ideas valuable – if you have any comments on them, please contact us by send an email to enquiries@propertyinvesting.net . They may be particularly helpful for people who might struggle with ideas and are better at the implementation-action-execution of property ideas. We will provide further listings of ideas if you think these are helpful – please provide feedback if you do. And forward them to your friends or colleagues if they catch your imagination.

- Invite a builder to do a deal on your property – cut of profits or provide incentive for low price building

- Prepare a list of renovation ideas for your portfolio then rank them on value, cost, time

- Provide bedsits for key workers or student houses anywhere where there is high yield e.g. Bradford, Woolwich, Plaistow, Kings Lynn

- Start a land acquisition agency – using website

- Buy a crescent flat in Buxton, Derbyshire – prices should rise strongly

- Buy land at auction or an old house and demolish for land to build big new executive house

- Get land and detailed planning permission for four – four story gated mews townhouses (with penthouse on top and terraces, do an off-plan development) – sell land with plans to developer

- Buy low cost un-renovated central City studios, renovate in high quality bachelor pad then flip

- Buy in Lille (High Speed One), Genoa (regeneration) and Prague (flats for £60,000, EU now joined)

- Manage your property yourself – save 15% on rental income

- Set up a trust fund for capital gains tax relief if you are an expatriate for 5+ years

- Gift property to your children if you have >£350,000 equity in your home, particularly if you are over 65 years old

- Specialize in high rental yield homes of multiple occupation - 4/5 bedroom London houses – make sure all tenants have jobs and good credit history.

By property in Bratislava (30 miles from Vienna ) and or Tatry Mts in Slovakia – boom area (low tax, car factories providing new employment)

By property in Bratislava (30 miles from Vienna ) and or Tatry Mts in Slovakia – boom area (low tax, car factories providing new employment) - By homes in Valencia – arts buildings/centre, architecture, night life, 3rd biggest Spanish city, new communications

- By property in Costa Blanca - looks like weather almost as good as Costa del Sol (dry, warm in winter) but much cheaper

- By property in Varna Bulgaria – has a nice beach, history, cheap villas and skiing 2 hours away – watch for expanding budget airline

- Do rental deal with local council to provide bedsits for key workers

- Buy land at the end of your garden – then build a house on it and sell – making serious profit

- Convert all lofts into extra rooms or flats

- Convert all basements into extra rooms or flats

- Extend all houses to double the size

- Build houses in the gardens of all detached properties with large gardens

- Use low cost property websites to sell property – saving 1.5% of sale price

- Buy house on corner plot, then build another house or extend to the side

- Have a housewarming party in your garden – invite your neighbours – then try and do some property deals with your neighbours who have large gardens

- Buy holiday home in Slovakia – cheap for summer breaks and very low priced

- Consider buying in Biarritz SW France – could be good holiday option (check flight costs etc) – nice food, weather okay, and up-and-coming

- Invest in property in Newquay, Cornwall – Rick Stein further north in Padstow, new Duchy Poundsbury, Fistral Surf Centre, rail investment, airport, Eden close by, baby boomers retiring and middle class surfing (boogie boards and better wet suits)

- Move to Slovakia to avoid tax – flat 22% tax rate and no capital gains tax on UK property sales after about 5 years

- Get grant from local council to build affordable homes

- Consider moving abroad for periods to maintain offshore tax status – and hence reduce 40% capital gains tax liability on sales

- Buy coastal bungalow, knock down, build on same floor plan with cellar, big dormer roof and attic rooms – build then sell on (or sell with plans attached)

- Do deals with a local architect

- Set up property consultancy and company to leverage your property skills and develop your passion – try to not do joint ventures (hence maintain control)

- Buy a farm just south-west of Calais in the hills close to the Eurostar (High Speed One) train station – could be new commuting area for London after 2010

- Buy in Bradford – fast growing property prices from low base (prices have doubled since 2002 and will likely rise with its proximity to Leeds )

- Consider buying land for a cemetery in UK in a nice location – there is a shortage.

The UK Budget

Nothing too shocking for the property investor in the budget. If anything, unlike last years SIPPs U-turn, this budget quietly gave some tax benefits to buy-to-let investors. For both UK and overseas property, you will now only be taxed on actual rental income instead of "intended" rental income (or the rental income of the tenancy contract). Hence if you have empty properties, you tax bill will be reduced. Also, for higher rate income tax earners, the new 20% banding (reduced from 22%) will be benefit since rental income is not subject to the increased national insurance payments on high income earners. For someone with a medium sized property portfolio earning about £44,000, this is likely to lead to a saving of some £1,500 per annum. It's probably an unintended consequence of fiddling with the national insurance and income tax rates (22 to 20% and scrapping the 10% bracket) – but all the same, every little bit helps.

UK Market Update

Rightmove reported a +0.9% rise in house asking prices in March in England and Wales. Highest increases were SE England (+2.1%), London (+1.8%), South-West (+1.9%), North (+2%) and West Midlands (+2%). Wales reported a drop of -0.3%. Prices in Southwark (+5%) and Lambeth (+4.1%) showed the biggest increase in London. Clearly the mini-boom continues though there are some early signs of a cool down. No sign of any crash as yet. The two recent interest rises to 5.25% seem to have had little impact as yet. It's likely rate rises will start to bite soon, particularly if rates rise to 5.5%. However, if and when they drop back again, it's likely to re-invigorate momentum. There could also be a shortage of homes on the market after June 1st 2007 when home information packs are introduced – some people think there will be a rush to sell properties before this date followed by a drought of properties for sale, because of the price of the HIPs. Read more ... in Special Report: 110: Which way the UK market - and why?

UK Interest Rates

CPI inflation is still 2.8%, predicted to drop to about 2% by year end. Oil prices have risen from $53/bbl to danger levels of $66/bbl. GDP is 0.7% in the last quarter – 2.7% in the last year. At midday Thursday 5th April, the Bank of England will announce their monthly interest rate decision. We put a 40% chance of a rise in April and a 40% chance of a rise in May. We think there is almost no chance of a rise in both months. We also think there is close to zero chance of a fall in interest rates in the next two months. So there is a very high chance in the next two months of a 0.25% rise – then likely staying at 5.5% for some months. Forward interest rate curves show 5.7% by end 2007 though these are normally 0.2% higher than actual levels. So expect 5.5% for the rest of 2007 in your cash-flow forecasts – we hope to see a 0.25% drop by year end, but it's looking less likely now oil prices have risen.

CPI inflation is still 2.8%, predicted to drop to about 2% by year end. Oil prices have risen from $53/bbl to danger levels of $66/bbl. GDP is 0.7% in the last quarter – 2.7% in the last year. At midday Thursday 5th April, the Bank of England will announce their monthly interest rate decision. We put a 40% chance of a rise in April and a 40% chance of a rise in May. We think there is almost no chance of a rise in both months. We also think there is close to zero chance of a fall in interest rates in the next two months. So there is a very high chance in the next two months of a 0.25% rise – then likely staying at 5.5% for some months. Forward interest rate curves show 5.7% by end 2007 though these are normally 0.2% higher than actual levels. So expect 5.5% for the rest of 2007 in your cash-flow forecasts – we hope to see a 0.25% drop by year end, but it's looking less likely now oil prices have risen.

Trends - Continuing Housing Shortage

Our website has been predicting a housing shortage for many years now and it's absolutely no surprise that the cumbersome planning process, increasing environmental constraints and land shortages, along with robust economic growth and increasing population has led to a severe housing shortage, particularly in southern England. This will remain. Cornwall has the biggest percentage increase in population of any county in the UK, but there is almost no new building. So is it any wonder prices continue to spiral upwards? London's population is due to increase by 800,000 in the next ten years – with the average household having two people per home, the city needs 400,000 new homes. We cannot see these being built either now or in the next ten years. What's more, most people want to live in proper home – e.g. a house with a garden. There are very few detached houses with gardens being built. So there is an increasing shortage of reasonable sized family homes with a garage, garden and close to good schools in southern England .

Our website has been predicting a housing shortage for many years now and it's absolutely no surprise that the cumbersome planning process, increasing environmental constraints and land shortages, along with robust economic growth and increasing population has led to a severe housing shortage, particularly in southern England. This will remain. Cornwall has the biggest percentage increase in population of any county in the UK, but there is almost no new building. So is it any wonder prices continue to spiral upwards? London's population is due to increase by 800,000 in the next ten years – with the average household having two people per home, the city needs 400,000 new homes. We cannot see these being built either now or in the next ten years. What's more, most people want to live in proper home – e.g. a house with a garden. There are very few detached houses with gardens being built. So there is an increasing shortage of reasonable sized family homes with a garage, garden and close to good schools in southern England .

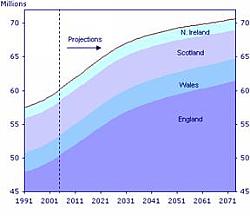

The population of England is due to increase from 46 million in 1990 through 50 million in 2007 to 58 million by 2040. The population of Wales and Northern Ireland will also grow strongly (see chart). For England, this implies an extra 6 million new homes being built between 1990 to 2040 – that's about 120,000 net new homes a year (on top of the 20,000 that are demolished). We frankly cannot see such high building levels being sustained to keep up with demand. From 2007 onwards, it's equivalent to increasing the housing stock from 26 million to 30 million – just to keep up – an increase of 15%. It's like building four cities the size of Manchester (2 million each). Meanwhile – the number of homes per person increased from 0.32 to 0.43 from 1961 to 1997. If this trend continues, by 2020 we'll need 0.55 homes per person – this statistic alone implies an extra 40,000 homes will be required on top of the 120,000 – hence 185,000 homes a year including those to replace demolished buildings. This is even more properties required, 4.3 million new homes by 2030 – again, we cannot see this happening.

So those houses that are not "shoe-boxes" are likely to see prices escalating at a healthy pace in the next few years. Used flats and Victorian conversion flats will also do very well – because of the reduced size of most families and more single people living alone. Particular shortages will occur in areas where fast growing economic activity converges with a lack of land, historic and pleasant surroundings and population increase, with minimal building. Examples include:

- Oxford

- Cambridge

- Brighton

- London – West End ( Chelsea , Soho, Belgravia , Kensington)

- London – west (e.g. Chiswick, Hammersmith)

- Winchester

- Guildford-Woking

- Reading

- Canterbury

- Maidenhead

- Bath

- Gravesend- NW Kent (new High Speed One Station)

- Truro

- Exeter

Baby-boomers downsizing and buying city centre properties in historic Cathedral Cities will drive the demand for higher-end apartments and quiet period terraces in such locations. Proximity to London will be important for these people – the above locations are examples of such locations. Read more ... in Special Report: 122: UK trends in services and manufacturing - how can I benefit?

UK South Coast Benefits

As the wealthy baby-boomers start to retire (some semi-retire) after 2010, many will head for home at the seaside but still want to be close to their business contacts and networks. As the UK warms up (global warming) the south coast is likely to become a more bearable place to spend winters and summers are likely to be rather warmer and drier if you believe all the talk on this. As oil prices rises, taxes rise for travel and airports become more congested, the south England resorts are likely to gain in popularity – the novelty of overseas travel might even wear off for some. But the key reason why this area will stay popular is because most UK nationals will want to stay at home because this is where their friends, family, employment possibilities

As the wealthy baby-boomers start to retire (some semi-retire) after 2010, many will head for home at the seaside but still want to be close to their business contacts and networks. As the UK warms up (global warming) the south coast is likely to become a more bearable place to spend winters and summers are likely to be rather warmer and drier if you believe all the talk on this. As oil prices rises, taxes rise for travel and airports become more congested, the south England resorts are likely to gain in popularity – the novelty of overseas travel might even wear off for some. But the key reason why this area will stay popular is because most UK nationals will want to stay at home because this is where their friends, family, employment possibilities  and investments are. A typical wealthy semi-retired baby-boomer is likely to have a property on the south coast, and spend time in London with old business contacts and fly out to the Alps for winter skiing and Spain or Cyprus for long summer holidays. They will not typically emigrate – because they'll see less of their families and friends and get bored quickly. So good quality coastal property in Southern England with a sea view and easy access to London will gain in popularity. Examples of good investment areas are:

and investments are. A typical wealthy semi-retired baby-boomer is likely to have a property on the south coast, and spend time in London with old business contacts and fly out to the Alps for winter skiing and Spain or Cyprus for long summer holidays. They will not typically emigrate – because they'll see less of their families and friends and get bored quickly. So good quality coastal property in Southern England with a sea view and easy access to London will gain in popularity. Examples of good investment areas are:

- Dorset: Poole, Swanage, Weymouth and westwards

- Sussex : Brighton, Eastbourne, Hastings , Portsmouth harbour, Chichester

- Hampshire: Bournmouth, New Forest

- Kent : Folkestone, Ramsgate, Broadstairs

- Cornwall: Penzance, Newquay, Truro , Rock, Helford River , Falmouth , Hayle, St Ives, Scilly Isles

- Devon: Torquay, Exeter , Plymouth harbour, Mindhead, Branscombe, Clovelly

- South Wales: Swansea , Gower, Barry, Pembroke, Tenby

Most of these towns face south making them warmer than they normally would be because they catch the sun. The sea keeps them warm in the winter and cool in the summer. In west Cornwall, temperatures are normally 3 or 4 degrees C higher than the Midlands in February. So if you can find large Victorian apartments with sea views or any home with a sea view and good aspect, it will likely rise in price more than average. It will also be easy to let out for holidays if it is in south-west England .

Most of these towns face south making them warmer than they normally would be because they catch the sun. The sea keeps them warm in the winter and cool in the summer. In west Cornwall, temperatures are normally 3 or 4 degrees C higher than the Midlands in February. So if you can find large Victorian apartments with sea views or any home with a sea view and good aspect, it will likely rise in price more than average. It will also be easy to let out for holidays if it is in south-west England .

Some market analysis: just imagine you are a middle class baby-boomer living in London or the Midlands (the total population of this area is some 30 million people). You are now 50-60 years old. You have £200,000 of equity in your home. You are retiring in the next ten years. Where will you want to live – Birmingham, Croydon, Milton Keynes? No, however you will likely want to be within reach of your family, friends, and old business contacts and therefore you will not move permanently abroad. You will want to be close to the beach or nice market town, preferably in an area where the weather is warmer than most of the UK. So forget high house prices – many of these people will clamber to buy property in Cornwall, Devon, Dorset, Hampshire, Sussex, Kent, coastal Essex, coastal Suffolk, Norfolk and coastal south Wales. The more wealthy may also have a pied-de-terre in London – as close as possible to the West End , Mid Town or City (e.g. Limehouse, Chelsea, Battersea, Kensal Green, Islington).

Some market analysis: just imagine you are a middle class baby-boomer living in London or the Midlands (the total population of this area is some 30 million people). You are now 50-60 years old. You have £200,000 of equity in your home. You are retiring in the next ten years. Where will you want to live – Birmingham, Croydon, Milton Keynes? No, however you will likely want to be within reach of your family, friends, and old business contacts and therefore you will not move permanently abroad. You will want to be close to the beach or nice market town, preferably in an area where the weather is warmer than most of the UK. So forget high house prices – many of these people will clamber to buy property in Cornwall, Devon, Dorset, Hampshire, Sussex, Kent, coastal Essex, coastal Suffolk, Norfolk and coastal south Wales. The more wealthy may also have a pied-de-terre in London – as close as possible to the West End , Mid Town or City (e.g. Limehouse, Chelsea, Battersea, Kensal Green, Islington).

What we do know is there is very little building of new homes in Devon, Cornwall and the best coastal stretches of Dorset, Suffolk and Hampshire. So prices are almost certain to rise. It's simply supply and demand. And those doubting Thomas's that say "we'll all be moving abroad" – sorry, we just don't buy this. Reason – family, friends, part time employment and health care (and the TV, football and all the cultural aspects). Most of these retiring baby-boomers will end up putting up with the bad weather and traffic jams on the motorways – because they'll want to be close to their family and friends. So properties in Cornwall or Devon and the south coast seem good investments . Spanish options will also likely do okay, but if you buy property in the UK, you won't have to pay 13% purchase and sale commission every time you make a transaction. Stamp Duty is a pain, but it's nothing like commissions and taxes in places like Belgium and Spain, particularly on lower priced property.

What we do know is there is very little building of new homes in Devon, Cornwall and the best coastal stretches of Dorset, Suffolk and Hampshire. So prices are almost certain to rise. It's simply supply and demand. And those doubting Thomas's that say "we'll all be moving abroad" – sorry, we just don't buy this. Reason – family, friends, part time employment and health care (and the TV, football and all the cultural aspects). Most of these retiring baby-boomers will end up putting up with the bad weather and traffic jams on the motorways – because they'll want to be close to their family and friends. So properties in Cornwall or Devon and the south coast seem good investments . Spanish options will also likely do okay, but if you buy property in the UK, you won't have to pay 13% purchase and sale commission every time you make a transaction. Stamp Duty is a pain, but it's nothing like commissions and taxes in places like Belgium and Spain, particularly on lower priced property.

From Repossessions to Buy-to-Let

The level of UK repossessions has risen significantly in the last year albeit from very low levels. But is this a serious issue? As interest rate rises have started to bite, in the lower priced areas where the lower income first time home buyer have overstretched themselves, there will be increasing levels of repossessions. In a normal market this might be a signal for house price to drop. But in the UK – it could be different this time. The reason is that many buy-to-let investors have very high net worth and cash reserves – and are likely to view these repossessions as opportunities to purchase property at below market value. So there will be a transfer of wealth from the distressed first time buyers to the large buy-to-let investors as some consolidation takes place. This type of consolidation is normal in business – the larger players who have the financial acumen, expertise and muscle will leverage their skills and help purchase property from distressed sellers that do not have these skills (otherwise they probably would not have got themselves into distress).

Because the population is rising, there is a housing shortage, employment remains strong, Gordon Brown has not hit investors with big tax hikes and the economy is strong – prices are not likely to drop but there will be more repossession opportunities. That said, the Banks need evidence (to prevent litigation) that the property has been properly marketed and is being sold at true market value – so repossessions do not  come at a discount in the current market. The best repossessions are properties that look tatty and superficially ugly (rubbish lying everywhere) but just need a good decoration to bring them back to normality. These properties might sell for £20,000 below similar well decorated properties, but only need a £2,000 tidy up and paint job. It's important to see through the mess and look at the fabric of the property – imagine what it would look like if properly decorated. I've yet to view a repossession that was not messy and needed re-decorating – and hence they normally sell for considerably less than normal properties.

come at a discount in the current market. The best repossessions are properties that look tatty and superficially ugly (rubbish lying everywhere) but just need a good decoration to bring them back to normality. These properties might sell for £20,000 below similar well decorated properties, but only need a £2,000 tidy up and paint job. It's important to see through the mess and look at the fabric of the property – imagine what it would look like if properly decorated. I've yet to view a repossession that was not messy and needed re-decorating – and hence they normally sell for considerably less than normal properties.

Major Development Areas

Areas with big construction projects, regeneration and new infra-structure normally rise in price at higher rates than more mundane suburban areas. In the south of England, there are some particularly important developments taking place which will transform the area – this is a list to highlight these for the canny investor.

- Stratford – Lower Lees Valley ( Olympics , High Speed One)

- Kings Cross (High Speed One)

Gravesend-Ebbsfleet (High Speed One, regeneration)

Gravesend-Ebbsfleet (High Speed One, regeneration) - White City ( Retail-Business Park )

- Wembley (Stadium-leisure)

- Greenwich peninsular (Housing)

- Docklands – from Limehouse to Beckton (Offices, housing, regeneration)

- Chiswick ( Business Park )

- London Bridge (general activity)

- Peckham (regeneration ongoing)

- South bank (latter phases of regeneration – from Vauxhall to London Bridge )

- Elephant & Castle (planned regeneration)

If you overlap all these development areas – it seems unlikely that places like Hackney Wick, Bow, Shoreditch , Canada Water, Stratford "village", Kings Cross and Borough will not see continued price movements higher. The 2012 Olympics, new High Speed One rail link, City Airport expansion and the sheer number of new higher paid jobs in the West End-City-Docklands corridor makes it a low risk investment area. We particularly like the area just south of Tower Bridge – prices drop quickly away from the Thames. The trick is to get a very well priced property as close to the river as possible but south of the river. All those city workers need crash pads somewhere – and this area of London, close to London Bridge railway station is becoming far more popular with the "city slicker" as years go by. If you can pick up a low priced flat just on the fringe of the main "building frenzy" prices will likely ripple out in the next few years.

If you overlap all these development areas – it seems unlikely that places like Hackney Wick, Bow, Shoreditch , Canada Water, Stratford "village", Kings Cross and Borough will not see continued price movements higher. The 2012 Olympics, new High Speed One rail link, City Airport expansion and the sheer number of new higher paid jobs in the West End-City-Docklands corridor makes it a low risk investment area. We particularly like the area just south of Tower Bridge – prices drop quickly away from the Thames. The trick is to get a very well priced property as close to the river as possible but south of the river. All those city workers need crash pads somewhere – and this area of London, close to London Bridge railway station is becoming far more popular with the "city slicker" as years go by. If you can pick up a low priced flat just on the fringe of the main "building frenzy" prices will likely ripple out in the next few years.  This zone started about ¼ miles south of the station. And remember, London Bridge is the site of the Glass Shard building planned to be London's tallest tower block, most likely to start construction shortly. This would add further kudos to the area – which benefits from Borough Market, the station (excellent communications), new offices, London Dungeons and proximity to the city.

This zone started about ¼ miles south of the station. And remember, London Bridge is the site of the Glass Shard building planned to be London's tallest tower block, most likely to start construction shortly. This would add further kudos to the area – which benefits from Borough Market, the station (excellent communications), new offices, London Dungeons and proximity to the city.

Macao - China

Interested in investing in a boom town? Macao is as close as you will get. The city used to play second fiddle to Hong Kong before China took control in 1999. High crime levels in the decaying ex-Portuguese colony did not help its cause. Since 1999, the Chinese authorities have driven most of the violent crime away and cleaned up the gambling business. The city now takes more gambling revenues than Las Vegas. £20 billion is being invested in regenerating the city and building huge new gambling casinos. It's expected the revenues will double by 2012 – mainly through Chinese people visiting the city. Along with this many new developments are springing up and a property boom is well underway. It's still a demanding place to do business, but for the experienced international property investor, it's worth considering.

US sub-prime lending issue

During the US property boom in the last 10 years, many banks lent money to borrowers with poor credit histories . When interest rates were a mere 1% in early 2003, payments were easy for these people. However, as interest rates rose to 5% up to 2007, these borrowers have been progressively getting into problems with payments. Many have drifted into arrears and some have had their properties re-possessed or handed back the keys. The glut of property in the poorer areas in the USA have seen property prices reduce – these are generally also the areas where many homes have been repossessed. It develops into a downward spiral. About 15 banks lending to sub-prime borrowers have gone bankrupt. This has affected the confidence of the property market. Because most US areas have ample land and building programmes, there is no shortage of properties for sale. Hence, when repossessions hit the market they tend to have a proportionately large impact on prices. That said, in most US areas, prices in Q4 2006 were still rising and the recent problems seem to be isolated into lower price suburban areas – in the poorer neighbourhoods. It's likely interest rates may not drop which will give a welcome boost to the property market. But there is a chance the current problems could get significantly worse. For experienced property investors, this could be a very good opportunity to purchase properties at well below true market value from distressed sellers – of course this is not without its risks because there could be a wholesale meltdown, but it's frankly unlikely and confidence could well return next year as the economy continues to grow and jobs are created in most US regions.

Oil Price – watch out

As previously discussed, we are on a monitoring brief on oil prices. Any oil price over $70/bbl signals problems – high oil prices increase inflation, lead to interest rate rises and can precipitate house price falls. Oil price are hovering around $66 / bbl at present, just below danger levels. We will keep you regularly posted on oil price developments – there is a possibility because oil production levels may be peaking and demand is rising, the supply/demand imbalance may cause prices to rise significantly, particularly if there are global security tensions. 25% of world oil supplies come through the Straits of Homez between UAE and Iran – if this area is blocked or threatened for any reason, oil prices would sky-rocket and this could precipitate a house price crash. An unlikely scenario, but it is possible. Any oil price below $50/bbl would be most welcome for property investors. If you want to hedge your position, it's a good idea to invest in oil towns – more detail can be found in Special Reports 56: Sophisticated Investors Follow Value - property, oil/gas, ore and gems! and 104: Oil & Gas How can I benefit from the boom?.

South Africa

The Football World Cup is planned for mid 2010. There will be new stadiums built and big infra-structure improvements in Jo'burg, Cape Town and other cities. The confidence this event will bring to the country will be great and property prices will likely follow upwards in the lead up to 2010. Property prices have doubled in the last few years and are expected to moderate to about a 10% increase this year. However, as in all the most desirable global areas, some parts of South Africa are likely to beat the national average. Examples include:

The Football World Cup is planned for mid 2010. There will be new stadiums built and big infra-structure improvements in Jo'burg, Cape Town and other cities. The confidence this event will bring to the country will be great and property prices will likely follow upwards in the lead up to 2010. Property prices have doubled in the last few years and are expected to moderate to about a 10% increase this year. However, as in all the most desirable global areas, some parts of South Africa are likely to beat the national average. Examples include:

Cape Town - Camps Bay , Bantry Bay , Seapoint, Cliftonville, Llandudno, Hout Bay , Wynburg

Cape Town - Camps Bay , Bantry Bay , Seapoint, Cliftonville, Llandudno, Hout Bay , Wynburg - Jo'burg

- Port Elizabeth (and the Garden Route to the west)

- Durban

No comments:

Post a Comment